The Decentralized Future of Work

I wrote last week about my experience working as a freelance consultant in the nascent industry around cryptocurrencies. It has not been lost on me that the independent nature of my efforts in this industry have, in many ways, reflected the focus on the individual that is inherent to bitcoin and its related technologies.

Many of the most influential people in cryptocurrency have made their contributions as individuals or as loosely affiliated groups. Bitcoin core developers, Ethereum contributors, angel investors, many prominent researchers, and Satoshi himself are all examples of individuals acting in place of any established, corporate efforts.

Decentralized systems lend themselves to this model of work. They enable payment and asymmetric upside for contributors that were previously impossible in other open source software efforts. The ethos and ideological underpinnings of these systems means that their development and their governance are most resilient when managed by a diverse group of independent actors as opposed to a single organization.

Aspects of this idea have been covered by others, notably Nick Tomaino’s The Slow Death of the Firm.

As I have found for myself, however, there are some aspects of the firm (and of central structure) that can be beneficial even to those who desire and choose to act as independent parties. In particular, leverage is missing. It is hard to act as a force multiplier when working alone and leveraged exposure to upside is hard to come by.

I outline below an idea for how the efforts of freelancers and individual contributors within the cryptocurrency ecosystem might be better structured and therefore leveraged — to the benefit of those contributors, to the benefit of projects, and to the benefit of the cryptocurrency ecosystem as a whole. Right now this is just an idea looking for feedback… and I would love to hear yours.

The Medieval period witnessed a breakdown of hierarchical systems. The centralized empires of the preceding centuries devolved into a sprawl of kingdoms, competing for territory, resources, hearts, and minds. These communities often had abundant financial resources, but manpower was hard to come by. In particular, seasoned military veterans were few and far between. Those soldiers who had seen previous action banded together into what became known as Free Companies. Free Companies were groups of experienced soldiers that worked for hire on behalf of communities, purveyors of services amidst the decentralized chaos of the Middle Ages.

Abstract

Teams aiming to ship cryptographic protocols are facing the problem of attracting top talent to work with them.

Meanwhile, many of the individuals working in the space would prefer to work broadly across the ecosystem. Additionally, these individuals often struggle to have upside correlated to the work they do with these projects.

The overall ecosystem is losing out because there are opportunities for collaboration and synergies across projects that are not being taken advantage of, as problems today are often solved behind the closed doors of individual projects’ headquarters.

There is an opportunity to bring together top multidisciplinary talent in a way that is in service of multiple protocol projects. There is also a way to reward this talent with stake in those projects.

From Centralized Systems to Decentralized Networks

Blockchain protocols are bringing about a shift in the way we interact and transact. These protocols replace centralized, trusted parties with decentralized, open networks of participants. The manner in which these protocols are being developed aims to reflect the technologies themselves: decentralized, open, and transformative.

Open source software projects are nothing new. They have thrived and created many of the systems that have come to shape society. As opposed to the mighty, preordained cathedrals of proprietary technology, open source projects have evolved in the fashion of bazaars with their own sense of order emerging out of chaos.

Blockchain protocols now represent the most well-funded open source projects in history. Over $6 billion has flowed into new protocol projects in 2017 alone. This is not to mention the astronomic appreciation of cryptocurrencies and tokens in the same period.

While many have lauded these projects’ abilities to fundraise, fundraising represents only the beginning. These projects, over the coming years, will face the far bigger and more important problem of shipping. To bring products and protocols to market, these projects will need teams of talent across an array of disciplines.

The Problem

Decentralized development has not yet found an effective framework. In particular it has not yet found a good way to match protocol projects’ demand for talent with those best positioned to ship. This is inefficient for the overall ecosystem, the projects themselves, and the individuals who contribute to these projects.

The Ecosystem

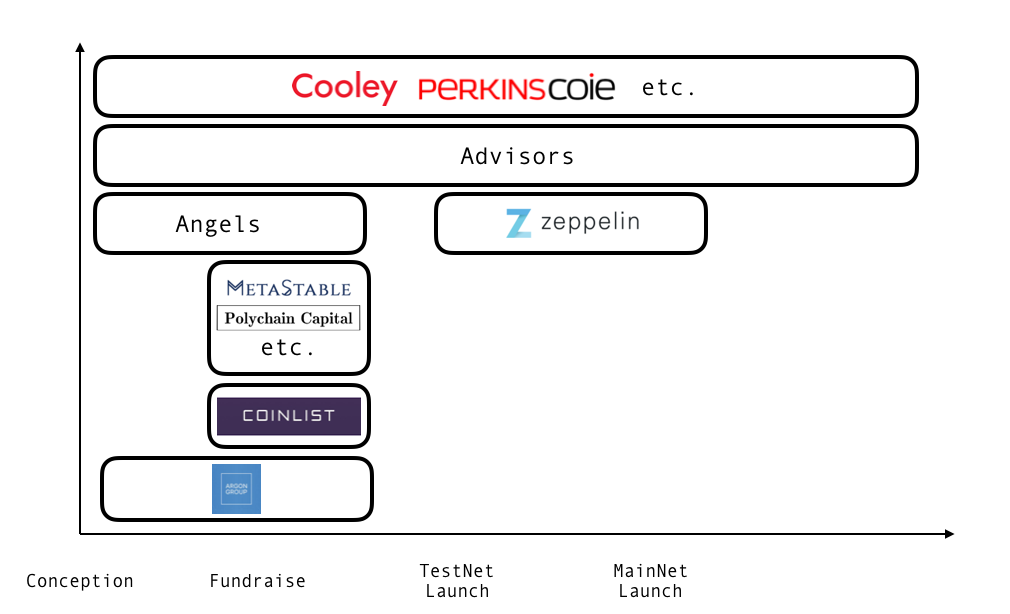

Broadly, the industry today is comprised of investors, project teams, and service providers.

Investors are concerned with seeing the projects they have backed ship the promised protocols and products. In order to do so, projects will need talented technical, product, partnership, legal, and marketing teams.

By and large, each project today is developing a team within its own silo. This is necessary for effective coordination and for achieving economies of scale. However, it can also run contrary to the promise of decentralization at the heart of many of these projects. After all, decentralized open source projects should draw from a broad base of contributors.

Each project developing within its own silo creates conditions for efficient roadmap development and management, but this comes at the expense of learnings and synergies that could be had across projects. Many of the challenges faced by any given protocol team reflect those faced by all the others. By seeking to solve these within their own walls, the opportunity to learn from each other and iterate gets lost. This is particularly ironic given the open ethos these projects aim to adopt.

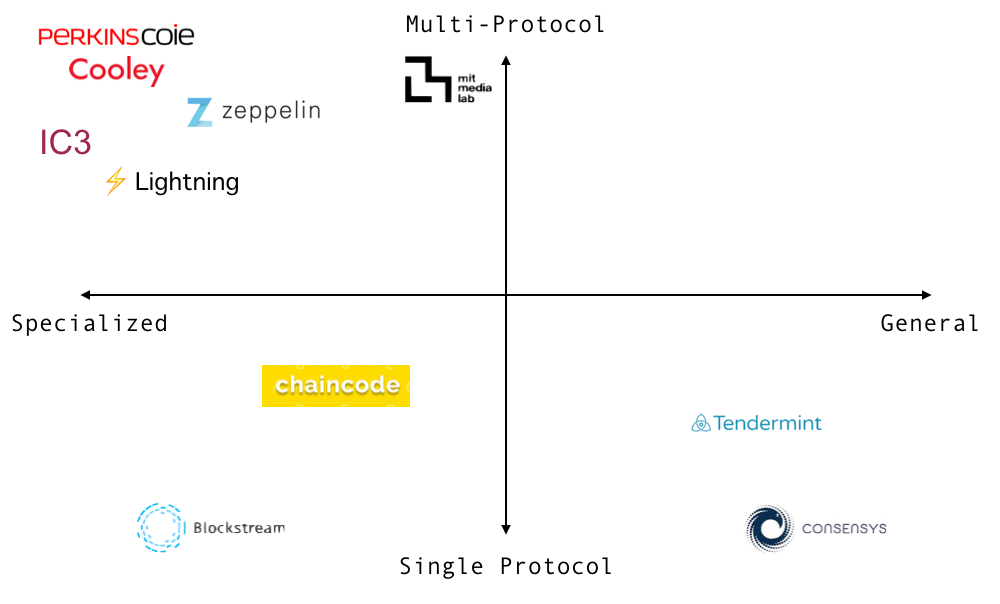

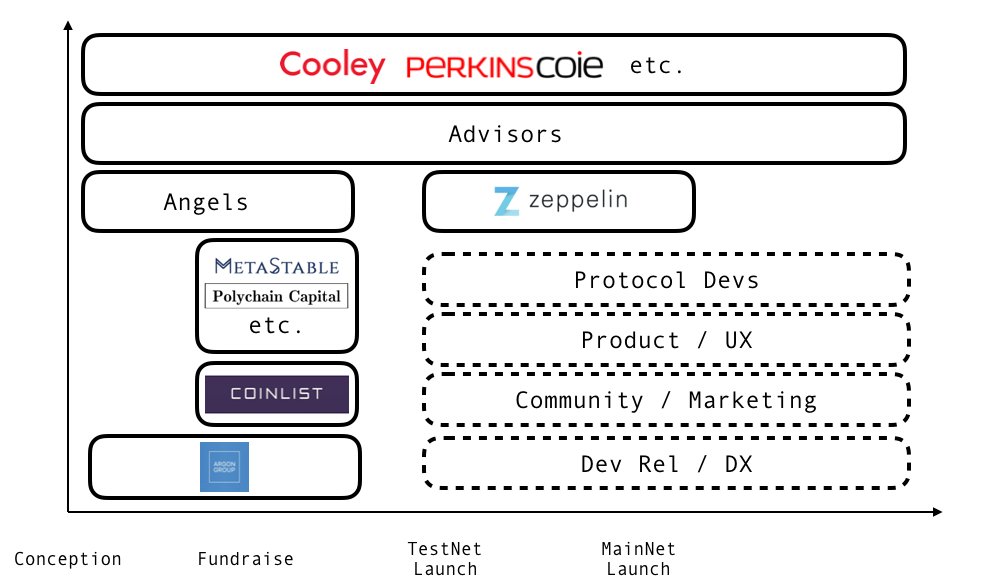

There is a broad array of service providers that work with one or multiple protocols.

Single-protocol service providers are often oriented around the development of either the core protocol or around the development of infrastructure and products built around or on top of that protocol. These groups are important for the decentralization of development, but continue with the same siloed approach of the individual protocol teams.

Multi-protocol service providers (advisors, academics, law firms, PR agencies, trade organizations) do some of the most important work across the ecosystem, but their approach is less than ideal for the multidisciplinary world of blockchain technologies, where questions of law, security, product, cryptography, and governance intertwine and speak to each other.

There are major synergies to be gained for the whole ecosystem by creating a team that works broadly across protocols and their problems. Most importantly, this model and the talent behind it will help projects meet that critical goal of shipping the decentralized protocols that they have promised.

Protocol Projects

Protocol projects now find themselves in a strong financial position, with funding ready to deploy towards innovation. This innovation spans:

Protocol development

- Research on mechanism design

- Experimentation with scaling solutions

- Implementations of STARKs

DX

- Work on virtual machines, compilers/transpilers, functional programming in smart contracts, high level languages

- Designing accessible IDEs

- Drafting solid documentation

- Defining best practices

- Developer education (boot camps, MOOCs, hackathons)

UI/UX

- Wallets (hard and soft; protocol-specific and multi-asset)

- Exchanges (in particular, the usability of decentralized exchanges)

- Decentralized application interfaces

- Browsers for tokens and dApps

Ecosystem development

- Partnerships with incumbents

- Bringing scaled payments solutions to decentralized marketplaces (e.g. Craigslist)

- Issuing assets on blockchain platforms (e.g. ticketing secondary market)

- Making the remittance use case a reality

- Partnerships with other protocol projects (E.g. Ethereum integration with Cosmos; Zcash collaboration with Quorum)

- Educating entrepreneurs and incubating projects

Legal

- Defining where cryptographic tokens lie within the legal frameworks of various jurisdictions

- Clarifying compliant distribution of cryptographic tokens

- Developing avenues for issuing legally-compliant cryptographically tokenized securities (and other asset classes)

- Creating standards for organizational structures and strong governance

- Advocacy and policy work

Marketing

- Developer relations

- Communicating the vision of cryptographic systems, blockchain technology, cryptocurrency to the public at large

- Communicating the visions of specific projects and protocols clearly, accurately, and accessibly

- These goals are shared across most protocol projects. These projects individually have the financial capability to execute on these initiatives.

These projects, however, face two critical challenges.

The first is the search for talent. Relative to present demand, there are few who would be considered experts or veterans of the space. This is certain to change with time, as individuals and incumbents see opportunity and pivot their paths to meet the demand. But the moat of understanding is large, particularly due to the multidisciplinary nature of blockchain technology, and it is early days.

The second challenge is the problem of how to balance efficient coordination with an ethos of decentralization. The culture of open source pervades these protocol projects. As such, the shape of teams necessarily looks different from historical, centralized, corporate structures. Concentrating too much power in the hands of a single figure or entity is often dissonant with the vision of the projects.

This question of how to achieve effective coordination and economies of scale in open, decentralized development remains open.

The Contributors

A major problem facing protocol projects is recruiting.

Working for or on just a single protocol is often suboptimal for the individuals best positioned to do so. Many of the most skilled, seasoned veterans of the industry believe strongly in the tenets of open source and would prefer to work on multiple projects. As outlined above, this is also suboptimal for the overall ecosystem. There are many synergies in the work being done across protocol initiatives, but the fractured system of competing fiefdoms that has emerged does not allow those synergies to be leveraged. This results in mass replication of work across projects (ironically, not dissimilar to the replicated work of miners in a proof of work system).

No one is more familiar with this replication of work than those individuals who work for service providers: law firms, security auditors, consulting practices, PR firms, and even executive coaches. These individuals and entities who work broadly across the space are some of the most critical contributors. Their birds’ eye view lends them a perspective and an ability to learn and iterate from project to project. However, these individuals often do not reap what they sow across the ecosystem, as their privileged positions do not always give them direct stake in the upside of the projects upon which they work (and in the case of lawyers can even preclude them from directly investing).

In fact, this problem of stake exists even for core developers on a given protocol project. Core developers, unless given grants of the cryptocurrency or tokens of the protocols they work on, do not have exposure to the projects to which they contribute (aside from their own capital that they put at risk in these assets).

Summary

So the state of the ecosystem is the following:

- There is little learning happening between siloed project teams despite opportunities for synergies and collaboration

- Protocol projects are the most financially well endowed open source projects in history

- Protocol projects are struggling to recruit due to overall low supply of talent, and what little supply there is being locked up in individual projects or as service providers

- Primary option for talented contributors who wish to work broadly across the space is contracting, but this is difficult to scale

- It is challenging for key contributors to fully participate in the upside of what they are delivering (without putting their own capital at risk)

- Projects need to ship and to do this they need to source contributors

- Contributors want to work in an open, decentralized, and collaborative manner

The Solution

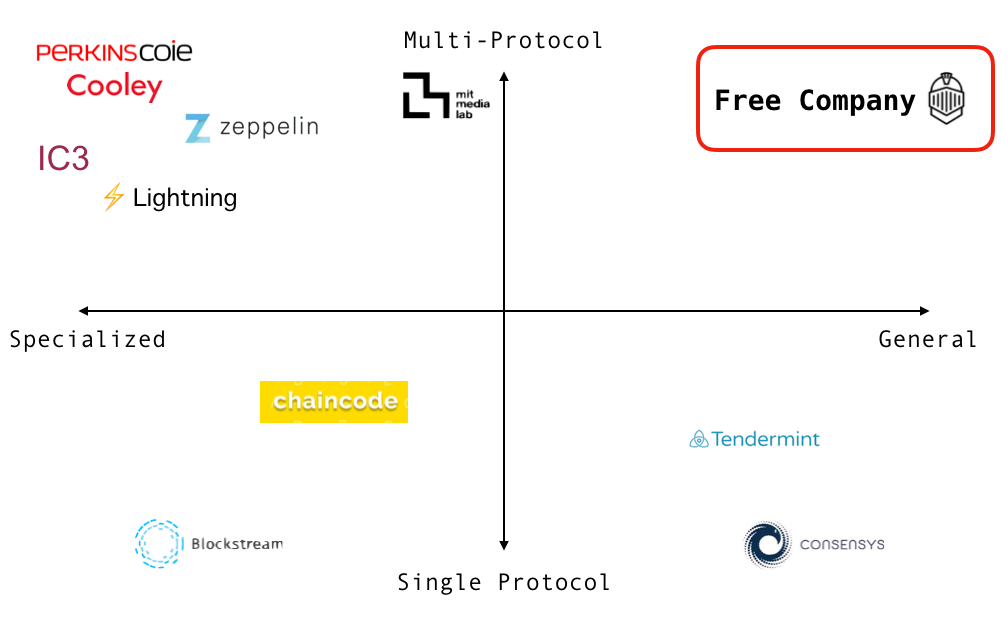

Free Company

The path forward is to create a system that can match this pent up supply of talent with the rampant demand from the projects. An entity or entities that will bring together top talent with top projects in the space, allowing contributors to work broadly across the ecosystem and allowing projects to gain from the spirit of open source. The solution is a Free Company that can be contracted to work on projects collaboratively across the space.

The idea of a Free Company is more than consultancy or services. It is about shipping, whether in the form of code, products, partnerships, educational initiatives, contracts, or content.

A Free Company would be about building, not signaling. A trend has emerged in the space for press releases to precede actual products. This is wrong and is a large contributor to major misunderstandings of the promises of cryptographic protocols.

A Free Company would focus on areas where there are synergies to be found, or opportunities to collaborate between projects.

A Free Company can fill a gap in the market right now, bringing talent together with promising protocol projects. It would be both multi-protocol and multidisciplinary, something no other service provider can currently claim.

A Free Company would also meet the most relevant demand in the market today (and what will remain the most relevant demand in the market for years to come). Service providers have emerged that service the earliest stage of projects (in the fundraising round), but have yet to emerge in force in service of these projects shipping.

Today, projects are solving the problem of shipping internally, in their respective silos. Few (if any) service providers work across protocol development, product, UX, community, marketing, ecosystem development, developer relations, and developer experience.

A Free Company could fill the gap of acting as a service provider across these various areas.

Finally, a Free Company would allow contributors to work in the manner they want: broadly, without non-competes, collaborating across projects and disciplines.

A Free Company can also provide upside to these contributors in a manner correlated with their contribution…

Bounty

A Free Company could also give contributors a stake in what they are building.

Revenue and upside would be generated in three manners:

Contracts with protocol projects

- A Free Company would be the go-to resource for protocol projects seeking to solve both specific (discrete) and broad (continuous) problems as they ship.

- A Free Company would also be a good diversifier for projects seeking to embrace the ethos of decentralization as they develop their technology and community.

Winning bounty programs put forth by projects

- On-chain bounties are increasingly being touted as the future of incentive-based development. These are devised as a way to reward developers with tokens based on their contributions to protocols. The teams who succeed in these bounties will likely be groups working collaboratively and also broadly across the space. A Free Company is well positioned to take advantage of these.

An investment fund that takes a stake in projects

- Investing in cryptocurrencies and tokens takes a highly multidisciplinary skillset. No cryptocurrency-focused fund today can say that its portfolio managers range across all relevant backgrounds and knowledge bases.

This investment fund could leverage the multi-disciplinary knowledge base and skill set of the contributors within the Free Company. Select individuals would serve as the investment committee of the fund.

- By drawing from top minds in protocol design, distributed systems, law, developer experience, programming language theory, use case analysis, marketing, and more, the fund can be uniquely positioned to succeed. But moreover, these contributors will have a stake in the future they are working to build.

- The fund would act as a separate entity and separately managed vehicle.

- Those working at the Free Company would be allocated GP interest / carry.

- The fund could be open to select outside LPs.

Summary

2017 was the year of the ICO, the token sale, the fundraise. The best way to capitalize in 2017 was to launch a project and to take money from investors: angels, individuals, venture capital.

That money has now moved from the hands of investors to the hands of protocol projects.

2018 is no longer about issuing assets. It is about building technology. The way to bring this about is to serve the projects, help them ship, and be among the builders shaping the decentralized future.